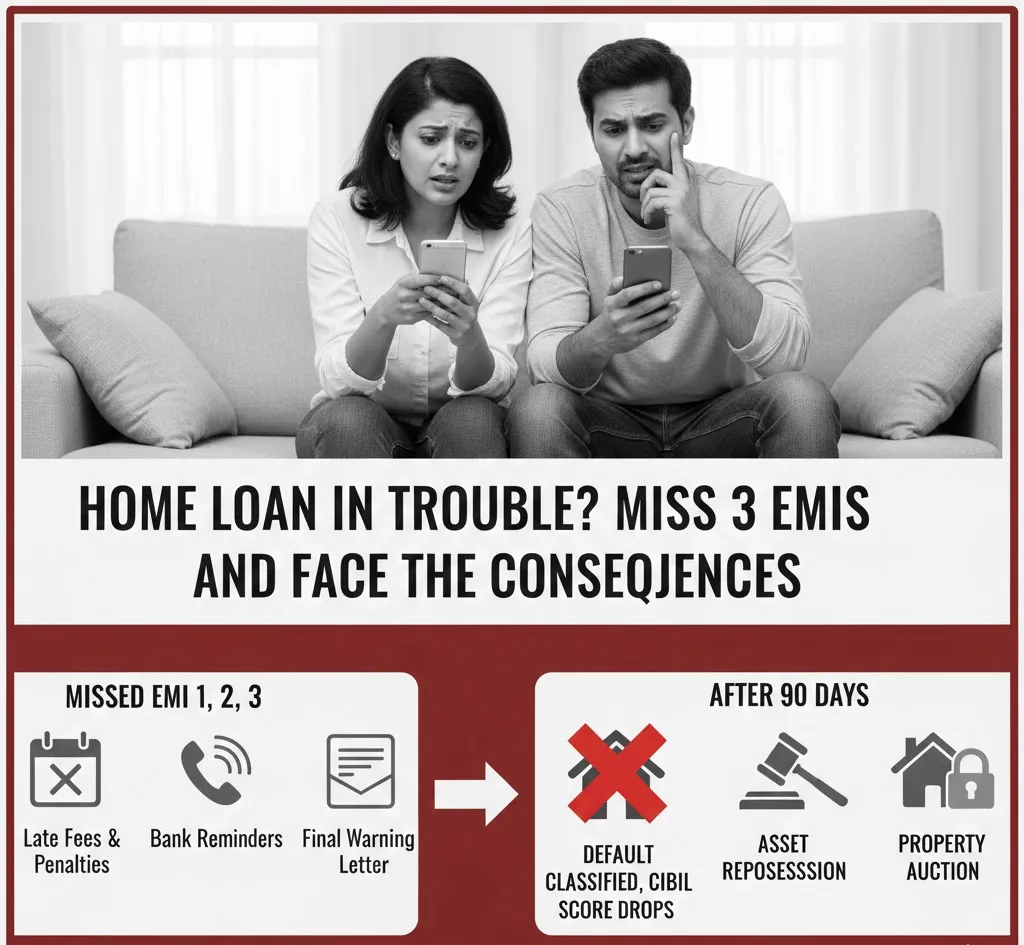

Taking ahome loanis a major financial commitment, and regular repayment ofEMIsis crucial to maintaining good financial health. Missing even one EMI typically starts with areminder from your lender, but repeated defaults can escalate quickly into serious consequences if not addressed promptly.

If you miss yourfirst EMI, banks send alerts and reminders, giving you time to regularise the payment without severe penalties. A second missed EMI moves your account into anoverdue category, which may result in the lender reporting the delay to credit bureaus, damaging yourcredit scoreand making future loans more expensive or difficult to obtain.

Missingthree consecutive EMIs (about 90 days)is a critical threshold. Under regulatory norms, the loan may be classified as aNon‑Performing Asset (NPA), and lenders can beginformal recovery action. This can include legal notices and initiation of recovery processes such as invoking theSARFAESI Act— allowing banks to take possession of and auction the mortgaged property to recover dues if the borrower fails to clear outstanding amounts.

In addition to recovery action, missing multiple EMIs attractslate payment charges, penal interest, and administrative fees, increasing your overall repayment burden. Yourcredit historymay be severely impacted, taking years of disciplined repayments to rebuild and affecting eligibility for future credit products.

Experts always advise borrowers who face financial difficulties tocommunicate early with lenders. Banks may offer loan restructuring, tenure extensions or temporary relief measures to help borrowers bring their accounts back on track. Proactive communication and early action can significantly reduce the risk of aggressive legal action or loss of your home.

ଉଚ୍ଚଶିକ୍ଷା ପାଇଁ ବଢ଼ୁଥିବା ଖର୍ଚ୍ଚ ଅନେକ ପରିବାରଙ୍କ ପାଇ...

କଳିଙ୍ଗ ଇନଷ୍ଟିଟ୍ୟୁଟ ଅଫ୍ ସୋସିଆଲ୍ ସାଇନ୍ସେସ୍ (KISS) ପର...

ଓଡ଼ିଶାର ସବୁଠାରୁ ବଡ଼ ରେଫରାଲ୍ ହସ୍ପିଟାଲ କଟକସ୍ଥିତ ଏସ୍ସ...

ରଥଯାତ୍ରା ଅବସରରେ ଶୈଳଶ୍ରୀ ବିହାର ଅଞ୍ଚଳରେ ଭକ୍ତଙ୍କ ବହୁ...

ଗଜପତି ଜିଲ୍ଲାର ମୋହନା କମ୍ୟୁନିଟି ହେଲ୍ଥ ସେଣ୍ଟର (ସିଏଚ୍ସ...

ବ୍ୟକ୍ତିଗତ କାରଣରେ ରାଜ୍ୟ ବାହାରକୁ କିମ୍ବା ବିଦେଶ ଯାତ୍ରା...

କଟକର ଏସ୍ସିବି ମେଡିକାଲ କଲେଜ ଓ ହସ୍ପିଟାଲ ପୁଣିଥରେ ଚିକିତ...

ଓଡ଼ିଶାରେ କୋଭିଡ୍-୧୯ ମାମଲାକୁ ନେଇ ଜନସ୍ୱାସ୍ଥ୍ୟ ବିଭାଗ ପ...

ରାଜଧାନୀ ଦିଲ୍ଲୀର ଜନ୍ତରମନ୍ତରରେ ଛାତ୍ରଛାତ୍ରୀଙ୍କ ବିରୋଧ...

ଦେଶବ୍ୟାପୀ ନିଟ୍ ପରୀକ୍ଷା ବିବାଦ ଓ ଶିକ୍ଷା ବ୍ୟବସ୍ଥାକୁ ନ...

ଉଚ୍ଚଶିକ୍ଷା ଅନୁଷ୍ଠାନଗୁଡ଼ିକରେ ନିଯୁକ୍ତି ପ୍ରକ୍ରିୟାକୁ ଅ...

ପବିତ୍ରବାହୁଡ଼ା ଯାତ୍ରା–୨୦୨୬ଅବସରରେ ଶୁକ୍ରବାର ପୁର...